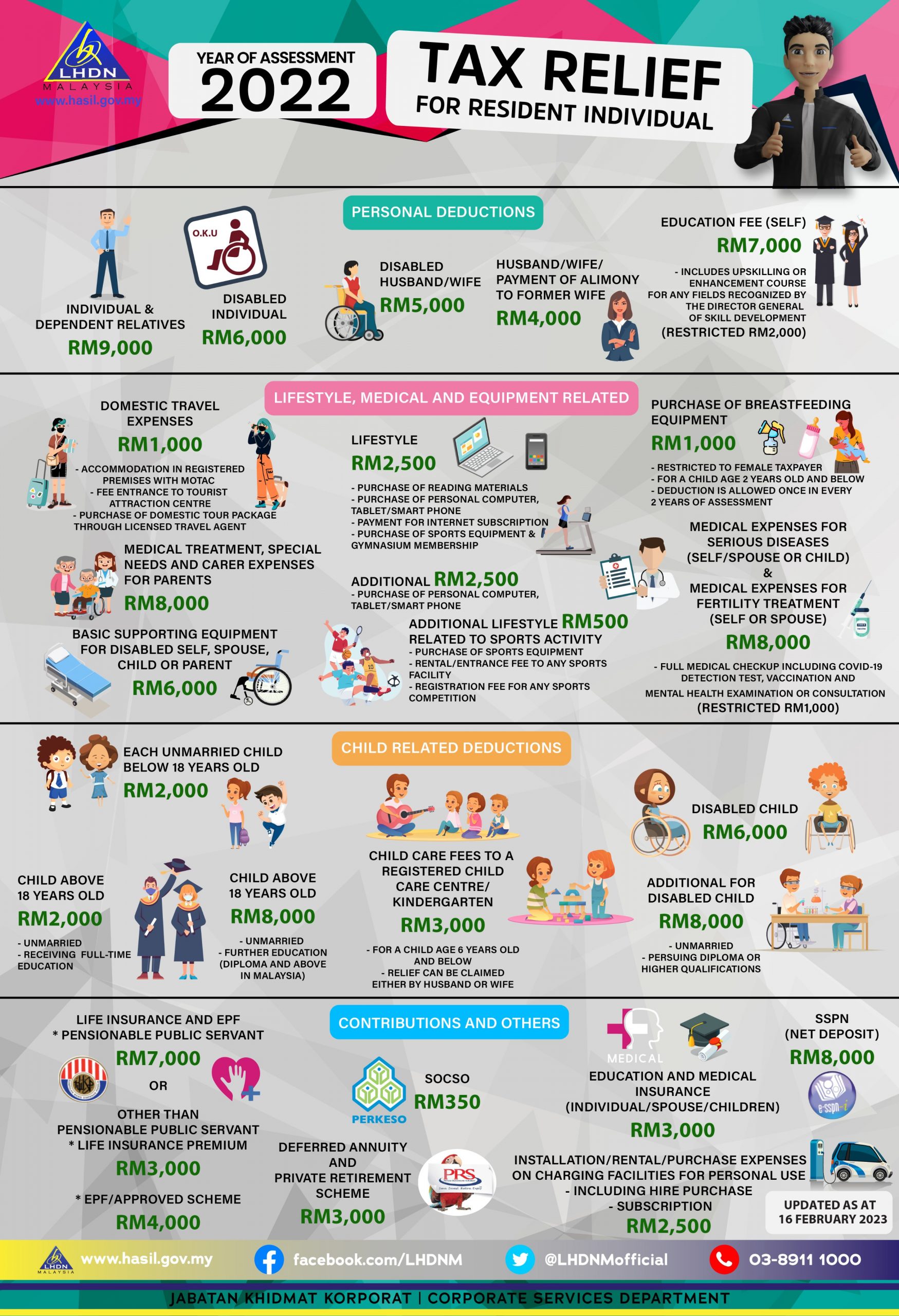

Types of Personal Tax Reliefs

A. Self –

1. Individual & Dependent Relatives: RM9,000

- Note that in the case of a married couple being assessed separately, both the husband and the wife will be able to claim a relief of RM9,000 each. There is no time apportionment of the relief, ie the full relief is also available even in the year of birth and the year of death of the individual.

2. Disabled Individual: Additional RM6,000

- A ‘disabled person’ is defined to mean any individual certified in writing by the Department of Social Welfare to be a disabled person.

3. Education Fees : Restricted to RM7,000

- This can be claimed on fees expended for any of the following courses of study undertaken in any institution or professional body in Malaysia recognized by the Malaysian Government or approved by the Minister of Finance:-

- (i) Other than a degree at Masters or Doctorate level

Any course of study up to tertiary level undertaken for the purpose of acquiring law, accounting, Islamic finance approved by Bank Negara Malaysia or Securities Commission, technical, vocational, industrial, scientific or technological skills or qualifications;

or - (ii) Degree at Masters or Doctorate level

Any course of study undertaken for the purpose of acquiring any skill or qualification. - For more details, please refer to the list of recognized local institutions or approved professional bodies in Malaysia at the official portal of the Ministry of Education Malaysia at https://www.moe.gov.my or

- (iii) Course of study undertaken for the purpose of upskilling or self-enhancement (Restricted to RM2,000)

8. Domestic Tourism Expenses: Restricted to RM1,000

(i) Payment of accommodation at the premises registered with the Commissioner of Tourism under the Tourism Industry Act 1992

For more details, please refer to the list of registered premises with the Commissioner of Tourism under the Tourism Industry Act 1992 at the official portal of the Ministry of Tourism, Arts and Culture at https://www.motac.gov.my/en/check/registered-hotel

(ii) Payment of entrance fee to a tourist attraction

(iii) Purchase of domestic tour package through a licensed travel agent registered with the Commissioner of Tourism under the Tourism Industry Act 1992

9. Expenses on charging facilities for Electric Vehicle (Not for business use) : Restricted to RM2,500

* Disabled Spouse: Additional RM5,000

C. Children

1. Child Relief – Unmarried child and under age of 18 years old (RM2,000 per child)

OR

Child Relief – Unmarried child of 18 years and above

– receiving full-time instruction (“A-Level”, certificate, matriculation or preparatory courses)

6. Net deposit in Skim Simpanan Pendidikan Nasional : Restricted to RM8,000

The allowable deduction is limited to the net amount deposited in that basis year only for his children. (Total deposits in 2022 – Total withdrawal in 2022)

Example 1:

Balance Brought Forward : RM4,500

Total Deposit : RM3,000

Total Withdrawal : RM2,500.

Allowable deduction is RM500 (RM3,000 – RM2,500).

The Balance Brought Forward of RM4,500 is not taken into account

D. Parent

Medical Expenses: Restricted to RM8,000

Parents refer to natural parents or foster parents where the individual is an adopted child.

Expenses on medical treatment for parents which qualify for deduction include:-

(i) medical care and treatment provided by a nursing home; and

(ii) dental treatment limited to tooth extraction, filling, scaling and cleaning but excluding cosmetic dental treatment expenses such as teeth restoration and replacement involving crowning, root canal and dentures.

Such claim must be evidenced by a medical practitioner registered with the Malaysian Medical Council (MMC) certifying that the medical condition of the parents requires medical treatment, special needs, or a carer.

E. Others

1. Lifestyle – for self, spouse or child: Restricted to RM2,500

Expenses for the use/benefit of self, spouse or child in respect of:-

(i) purchase of books/journals/magazines / printed newspapers / other similar publications, whether in the form of hardcopy or electronic (Not banned reading materials)

(ii) purchase of personal computer, smartphone or tablet (Not for business use)

(iii) purchase of sports equipment for sports activity defined under the Sports Development Act 1997 (e.g. golf balls and shuttlecocks but EXCLUDING motorized bicycles) and payment of gym membership

(iv) payment of the monthly bill for internet subscription (Under own name)

2. Lifestyle – Tech: Restricted to RM2,500

Additional relief for the use/benefit of self, spouse or child in respect of:

Additional deduction for purchase personal computer, smartphone or for own use/benefit or for spouse or child and not for business use

3. Lifestyle – Sports: Restricted to RM500

Additional relief for the use/benefit of self, spouse or child in respect of:

(i) Purchase of sports equipment for any sports activity as defined under the Sports Development Act 1997

(ii) Payment of rental or entrance fee to any sports facility

(iii) Payment of registration fee for any sports competition where the organizer is approved and licensed by the Commissioner of Sports under the Sports Development Act 1997

4. Medical expenses for serious diseases for self, spouse or child: Restricted to RM8,000

(the expenses incurred for vaccination and medical examination can only be RM1,000, out of total RM8,000)

Serious diseases include the treatment of:-

- Acquired Immune Deficiency Syndrome (AIDS)

- Parkinson’s disease

- Cancer

- Renal failure

- Leukemia

- other similar diseases (include heart attack, pulmonary hypertension, chronic liver disease, fulminant viral hepatitis, head trauma with neurological deficit, tumour in brain or vascular malformation, major burns, major organ transplant and major amputation of limbs.)

Receipt of the treatment and a certification issued by a medical practitioner registered with the Malaysian Medical Council (MMC) must be kept for future reference and inspection, if required.

5. Medical expenses for fertility treatment for self or spouse

6. Vaccination for self, spouse and child (Restricted to RM1,000)

7. Medical expenses on:- (Restricted to RM1,000)

(i) Complete medical examination for self, spouse or child

Complete medical examination refers to thorough examination as defined by the Malaysian Medical Council (MMC).

(ii) COVID-19 detection test including the purchase of self-detection test kit for self, spouse or child

(iii) Mental health examination or consultation for self, spouse or child

8. Basic supporting equipment for disabled self, spouse, child or parent: Restricted to RM6,000

This deduction is only allowed for the purchases of basic supporting equipment to the disabled individual (self, spouse, child or parent) who is registered with the Department of Social Welfare (DSW) as a disabled person.

Basic supporting equipment includes haemodialysis machine, wheel chair, artificial leg and hearing aids but excludes spectacles and optical lenses.

9. Education and medical insurance: Restricted to RM3,000

This deduction available on insurance premiums in respect of education or medical benefits for an individual, husband, wife, or child.